We often hear excuses from young parents that they don’t save because their savings would push them into a higher income class and they would receive a lower child allowance per month as a result. The reason for the decision against saving is generally unfounded because such savings are taken into account only in the form of fictitious interest.

Example of calculation for a 4-member family:*

The annual income of a family of four is 32,400 EUR. Mother and father formed a liquidity reserve of 15,000 EUR, which they keep in a savings account, and saved 10,000 EUR in mutual funds through a savings plan.

| Annual income | Total assets | ||

| Mother | 14.400 | Cash in savings account | 15.000 |

| Father | 18.000 | Cash in funds | 10.000 |

| Total | 32.400 | 25.000 | |

| Total amount of income | |||

| Annual income | 32.400 | ||

| Interests on assets (0.37% of the value of assets 25.000 EUR) | 92,5 | ||

| Total | 32.439 | ||

| Monthly income per family member (excluding assets) | 675 | ||

| Monthly income per family member (including assets) | 677 | ||

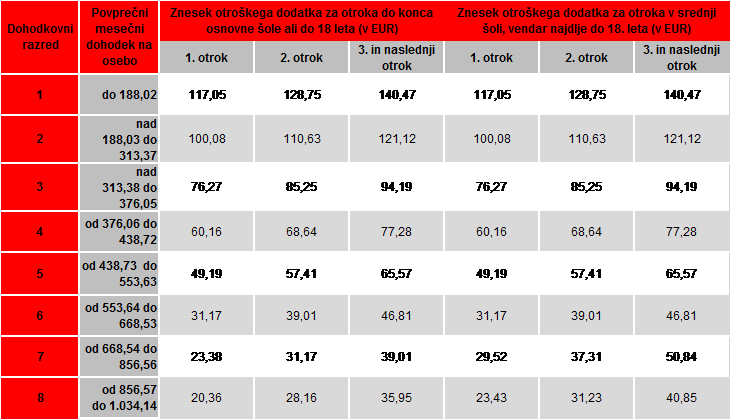

The above calculation shows that the monthly income per family member (32,493: 12: 4 = 677), taking into account the savings, is only 2 EUR higher than the income without taking into account the assets. According to the calculated monthly income, the family is classified in the 7th income class.

Source:

Source: Explanation – which income and property affect the amount of social transfers or kindergarten fees?

In determining entitlement to child allowance, reduced kindergarten fee and state scholarship, the following is taken into account:

- Income received in the previous calendar year before submitting the application, based on the personal income tax assessment decision;

- Movable and immovable property: real estate, personal and other vehicles, watercraft, ownership shares of companies or cooperatives, securities, money in a transaction or other account, savings deposits and other cash at the request of an individual and other movable property.

Total assets (not considered for all assets equally) are considered by adding to the income of the applicant and his family the amount they would have received in one year from interest calculated on the value of the assets (on the date of application) if they had the amount in the value of the assets deposited in a bank account in the form of a time deposit. The average annual interest rate for households for time deposits over 1 year up to 2 years for the year before the year of application is considered, according to the Bank of Slovenia. In 2017, the interest rate was 0.37 %, in 2016 0.51 %, in 2015 0.96 % and in 2014 1.9 % (source: Bank of Slovenia). As an additional reduction in interest rates is expected, we can assume that all savings will have an even lower impact on the amount of social transfers.

We can conclude that saving at a bank, mutual funds or other securities has very little effect on the calculation of monthly income per family member and consequently also on the amount of social transfers received.

*For ease of understanding, only investments are taken into account in the calculation; otherwise, other assets are taken into account. A further 48 multiple the minimum income is deducted from the total value of the assets, and then the fictitious income of this property is calculated.

Back